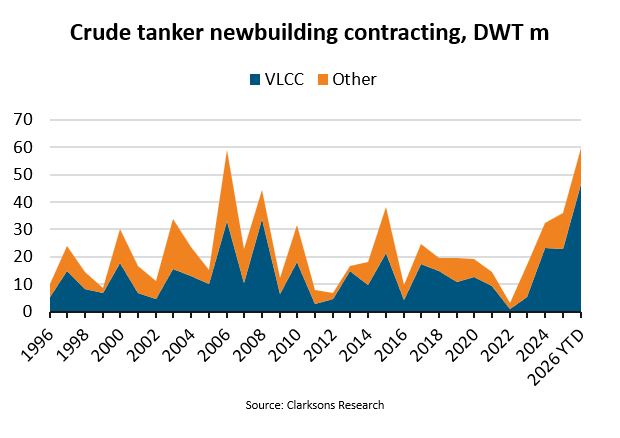

Crude tanker newbuilding contracting hits record high at 60m DWT

“So far this year, crude tanker newbuilding contracting has reached 60m deadweight tonnes (DWT) across 234 ships, driven by a surge in orders for Very Large Crude Tankers (VLCCs). This already makes 2026 the year with the highest crude tanker contracting on record. High freight rates and the need to replace an increasingly older fleet have both encouraged contracting,” says Filipe Gouveia, Shipping Analysis Manager at BIMCO.

Orders for new VLCCs are already more than double than in the whole of 2025. A total of 151 VLCCs have been ordered so far this year, accounting for 79% of contracted crude tanker capacity. Most of the remaining new orders consist of ships in the suezmax segment, and these have already reached the capacity ordered during the whole of 2025.

“The total crude tanker order book has now hit 130m DWT, the highest on record and equivalent to 27% of the current crude tanker fleet. With deliveries scheduled through 2030, new capacity entering the market is set to gradually increase until at least 2028. That would mark a sharp acceleration from the less than 10m DWT delivered annually over the past three years,” says Gouveia.

The increase in ship deliveries is expected to contribute to the crude tanker fleet’s renewal. The fleet has been gradually aging since 2011, amid slowing deliveries and low ship recycling, and the average ship is now around 14 years old. Tankers are typically designed to operate for 20 years, but 22% of the current fleet, accounting for 105m DWT, are now older than that.

Out of the ship capacity contracted so far this year, only 2% is expected to use alternative fuels, mainly LNG, while an additional 17% is being designed to allow for future retrofitting. This is a slowdown in contracting of crude tankers using alternative fuels, since in the whole orderbook, 9% of ships are expected to use alternative fuels, while an additional 30% can be retrofitted.

Chinese shipyards have continued to be the preferred choice for new crude tanker orders, accounting for 82% of ordered capacity so far this year. In the current order book, Chinese shipyards account for 70% of ordered capacity, while Korea takes an additional 25%, with a greater focus on the suezmax segment.

“Looking ahead, crude tanker newbuilding contracting could begin to slow down. The order book is already large and lead times are high, with recently-ordered ships only expected to be delivered after two to four years. And the timeline for when transit conditions in the Strait of Hormuz return to normal remains uncertain, thus clouding the market outlook for crude tankers,” says Gouveia.