Clarksons Research issues update on Middle East situation’s impact on shipping markets

Clarksons Research, the data and analytics arm of the Clarksons Group, has been closely monitoring shipping activity and markets impacted by the conflict. With hostilities now in their fourth week and transits through the Strait of Hormuz down 95%, the company’s Global Head, Steve Gordon, comments as follows on the effect on shipping markets:

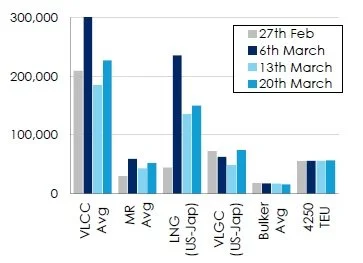

Vessel charter rates across tanker and gas remain elevated despite loss of cargo volume, with a range of ‘mitigating’ factors currently lending support (see graph of market indicators, in $/day, source Clarksons Research).

Energy shipping markets for now remain at elevated levels (VLCC earnings at $227,000/day, MRs $52,000/day, LNG firmer w-o-w, rising to $150,000/day, VLGCs up to $74,000/day). Bulk carrier earnings are steady for now ($15,000/day), while container freight rates have edged higher (knock-on logistical disruption has so far been more limited than initial expectations and rates remain well below Covid-19 levels)

The cost of moving a barrel of crude oil remains elevated at $10/bbl (on a US Gulf - Asia voyage), up from $5/bbl at the start of the year.

High bunker prices (e.g. VLSFO in Singapore stands at ~$1,000/t, >100% vs start-26) amid oil supply shortages - our data suggests that average container vessel speeds are down 2% across March so far.

Prior to the conflict, 20% of global oil supply passed through the Strait of Hormuz, including 37% / 19% of seaborne crude oil and products trade. 19% of global LNG trade (3% of global natural gas supply) also passed through the Strait, alongside 28% of global LPG volumes (~10% of supply), as well as 13% of seaborne chemicals, 9% of cars, 4% of dry bulk and 3% of container trade volumes.