Straits of Hormuz transits remain 95% down: Clarksons

Clarksons Research, the data and analytics arm of the Clarksons Group have been closely monitoring shipping activity and markets impacted by the conflict.

Summarising their latest update issued at 10.00 am yesterday (16 March), Steve Gordon, Global Head of Clarksons Research detailed as follows:

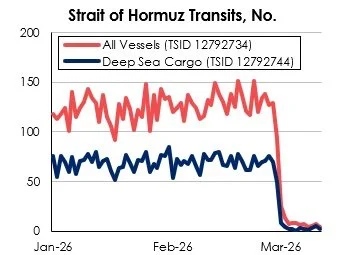

Strait of Hormuz transits are down 95% on pre-conflict levels (at an avrage 5 transits per dayover the past week vs around125 pre-conflict, with 80% of transits having been exiting the Gulf in the past week.

Just 3 oil tankers with ~2m bbl capacity passed through the Strait across the weekend (vs 40 tankers over a typical two-day period), alongside 2 Indian-linked VLGCs while no LNG carriers have passed through the Strait in March.

Excluding locally trading vessels, there are ~1,100 ships (37m GT of $30bn) currently inside the Gulf. This total features ~250 oil tankers, including 5% of crude tanker (7% of VLCCs) and 3% of product tanker tonnage as well as 4% of VLGC and 1% of containership and bulker tonnage.

Some alternatives to Strait of Hormuz are developing: VLCCs en-route to Yanbu on the Red Sea are up sixfold; IEA’s 400m bbl stock release draw has begun in Asia.

Charter rates for tanker and gas carriers eased through last week, though generally remained very elevated. Average VLCC earnings stood at $185,000/day (x5 long-term averages) on Friday, while LNG carrier spot rates stood at a firm $135,000/day (+45% vs long-term trend) and VLGC earnings on the US-Japan route eased week-on-week but showed resilience at $48,305/day (-7% vs 10-yr avg.). Bulker and container markets have seen more limited impacts for now.

The cost of moving a barrel of crude oil remains elevated at $10/bbl (on a US Gulf - Asia voyage), up from $5/bbl at the start of the year.